Why you shouldn’t take the car dealership loan offer!

Simply put:

When you finance through a bank/credit union you pay off more principal than interest. When you pay through the dealership you pay more interest than loan.

Simple explanation:

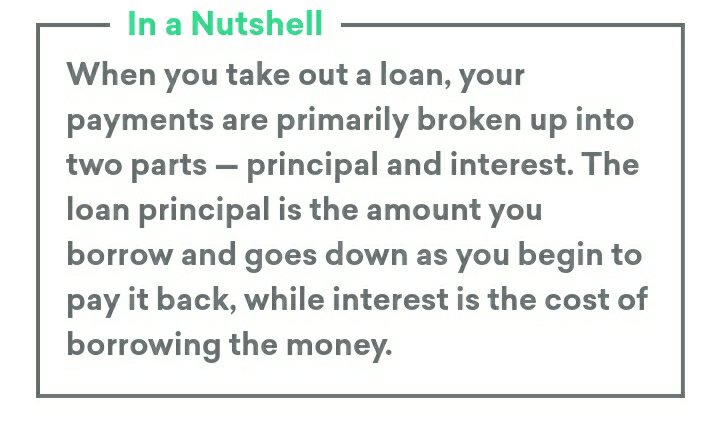

There are two different things you pay when you pay for your car loan.

- Interest on the loan

- Principal on the loan (the meat of your loan aka the price of the car itself)

Car dealerships and car companies are absolutely willing to give you great interest rates and they may match the banks however,…. They don’t tell you that you’re paying way more interest than the car principal. In extreme scenarios, you could be paying exclusively interest depending on what you’re dealership doesn’t tell you!

Imagine paying for your car for 2 years and you haven’t touched your principal balance!! This means you’re car loan is literally the same until you pay all the interest first. This could take years to do depending on your contract.

This is BAD if you plan to trade-in the car in a few years. You’ll owe that same amount you took a loan for and definitely be upside down (owe more than the car is worth). While your car has depreciated, you will not have paid any principal only interest.

Simple note:

Please read the fine print! This is essential to see exactly how much principal and interest your payment consist of. This goes for new or used!

Simple statistics:

Car dealerships are more likely to give you a payment ratio of 70-30 (interest – principal). Some have been reported as high as 98-2 where nearly all the payment is interest based with little to no principal.

That is unacceptable and will guarantee that you will be upside down on your loan. The average vehicle depreciates by roughly 2% each month for the first couple of years (varies depending on current trends).

Banks on the other hand are inclined to normally allow near 50–50 and lower interest with more principal. We’ve seen the be around 80-20 (principal-interest). This will result in a car that’s nearly paid for come trade-in time.

Simple example:

Bank/credit union loan:

Let’s say you want a $20K car.

The bank offers you 10% interest for 72 months. That’s about $26K total and about $371a month.

By the typical 70-30 (principal-interest) ratio of BANKS/CREDIT UNIONS that’s about $260 to principal and $111 to interest.

4 year balance:

$12480 – principal

$5328 – interest

Total Paid – $17808

Car principal remaining – $13520

Vs

Car dealer loan:

The same $20K car but the dealership offers 5% interest over 72 months (side note, I use a lower interest rate because some salesman will get a lower amount as a way to get your business!).

That’s $23K total and about $322 a month.

Many would be favoring the dealership. Now let’s apply the aforementioned typical dealership ratio of 70–30 (interest-principal).

That’s $225 to interest and $98 to your principal amount!

4 year balance:

$10800 – interest

$4704– principal

Total paid – $15504

Car principal remaining – $18296

Vs

Bank/credit union loan same interest:

$20K car. 5% interest for 72 months. That’s about $23K total and about $322 a month.

By the typical 70-30 (principal-interest) ratio of BANKS/CREDIT UNIONS that’s about $225 to principal and $98 to interest.

4 year balance:

$4704– interest

$10800– principal

Total paid – $15504

Car principal remaining – $12200

Simple math:

Compare to the above numbers. Yes, one of the bank/credit union loans paid more but even at the same percentage rate of 5%, the person who chooses the dealership funding looses out on thousands over the years. Come trade in time, the bank/credit union has set whomever up nicely!

Bank (high interest) – $13520

Dealership (5%) – $18296

Bank (5%) – $12200

The principal amount is the main amount that you want to pay off. Yes a higher percentage means you have to pay more over time, but the average person trades in a vehicle every 2-3 years in modern times. That’s not much.

Based on the above examples, having a higher interest rate evens out very quickly. Please look at your local banks and credit unions first before going to the dealership.

Simple Sense:

Even at a DOUBLE DIGIT percentage, it’s BETTER than paying more interest principal!

Simple note:

Ratios subject to vary based on your credit rating and other factors. No two rates will be the same for people, even with an identical credit score. Various factors go into these and taxes and fees come into play as well as down-payment and a laundry list of other factors. We advise credit unions as they offer a variety of good payment options and can really work with you.

Simple conclusion:

The numbers speak for themselves, but just incase… Take the credit union. It’ll literally save you thousands and keep you in good terms come trade-in time. You’ll get the same haggle price and you will be much happier as the years tick on.

Do you ever read the fine print when you get new things or sign up for offers?